Insurance underwriters across the Gulf spend a substantial share of their workday on data entry, document chasing, and manual rule-checking — not on actual risk decisions. That’s a well-known operational drag in the MENA insurance industry, and it’s exactly what AI automation is now beginning to dismantle.

AI automation for insurance underwriting workflow MENA refers to the use of intelligent software agents to ingest, validate, price, and approve insurance applications across Middle East and North Africa markets — automatically, with human oversight at the decision points that matter. Vendors active in the region, including eData and mea Platform, publish marketing claims of up to 90% fewer errors and 40%+ more in-appetite business written. These are vendor figures, not independently audited results — we treat them as marketing claims throughout this article and explain how to verify them for your own book. The shift toward operational deployment is real, but the headline numbers deserve scrutiny.

A note on sourcing and scope: this article is written from a vendor-neutral, practitioner’s standpoint. Where it describes implementation patterns, those are framed as what teams building these systems generally encounter — not as proprietary first-party results. Every statistic is attributed to its original publisher so you can check it yourself.

Quick Summary: AI Underwriting Automation in MENA

- What it is: AI underwriting automation in MENA uses multi-agent AI systems to automate the four-stage underwriting workflow — ingest, validate, apply rules, and trigger actions — across Middle East and North Africa insurance markets. These systems supplement manual document review and rule application with coordinated AI agents that process submissions end-to-end, while keeping humans at the decision points.

- Error reduction (vendor claim): eData, a MENA-focused automation provider, claims up to 90% fewer error margins after deploying multi-agent underwriting (eData, LinkedIn, October 2025). This is a marketing figure, not an independently verified benchmark.

- Business uplift (vendor claim): mea Platform states its Intelligent Underwriting products help underwriters write “over 40 percent more in-appetite business with no extra effort” (mea Platform / Financial IT). Again, a vendor claim.

- Regional requirement: Compliance with Saudi Arabia’s SAMA and the UAE’s insurance regulator, plus Sharia-compliant Takaful logic, is non-negotiable.

- The real challenge: Arabic-language document processing and dialect handling — where many platforms designed for Latin-script inputs struggle.

- Build vs. buy: Custom AI agents tend to win on ERP integration and Takaful compliance; off-the-shelf tends to win on speed-to-deploy.

Published: 27 June 2026. Last updated: 27 June 2026.

What Is AI Automation for Insurance Underwriting Workflow in MENA?

AI automation for insurance underwriting workflow MENA is the deployment of specialized AI agents that handle the end-to-end underwriting lifecycle — from application intake to risk pricing to compliance approval — tailored to Middle East regulatory and linguistic requirements. The dominant emerging paradigm is agentic AI, where multiple specialized agents collaborate across the process.

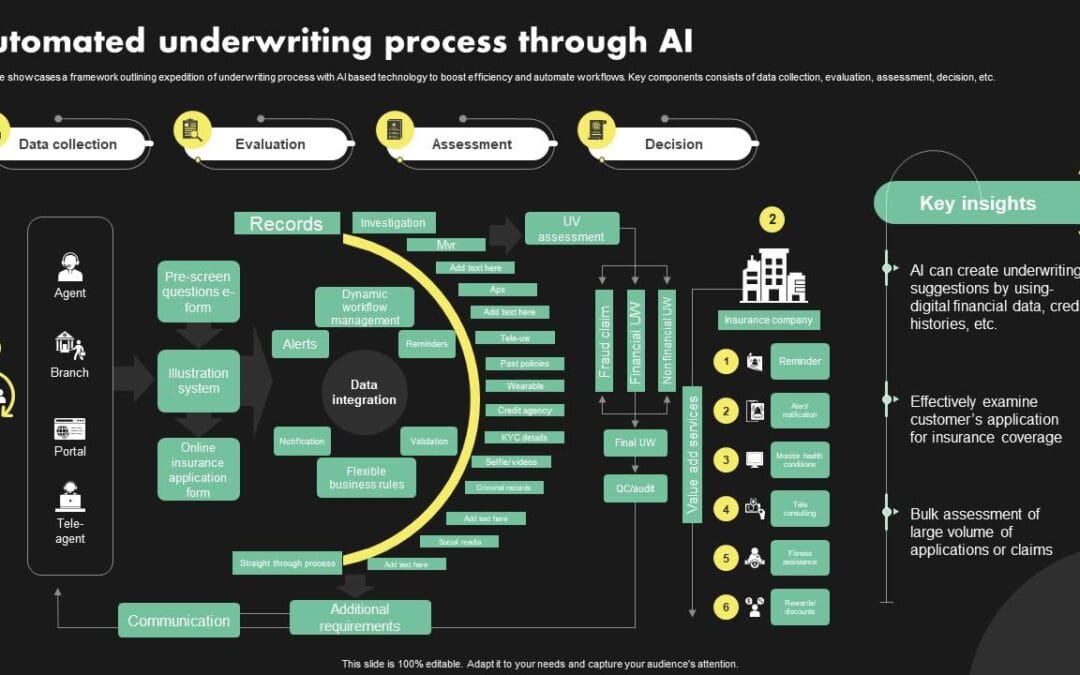

The standard automated underwriting workflow is commonly described in four stages:

- Ingest: Pull data from applications, broker submissions, medical reports, and actuarial models — including unstructured PDFs and Arabic-language documents.

- Validate: Check the data for completeness, accuracy, and fraud signals before anything moves forward.

- Apply rules: Run the insurer’s underwriting guidelines, risk appetite, and Sharia-compliance constraints against the validated data.

- Trigger actions: Auto-approve, auto-decline, route to a human underwriter, or request additional documentation.

According to InsurTech Gulf, agentic AI “deploys multiple specialized agents across the underwriting lifecycle — intake, risk profiling, pricing, compliance, and decision orchestration.” Rather than one monolithic model, each agent owns a narrow task and hands off cleanly. That separation matters for auditability, which MENA regulators demand.

Key terms defined. Agentic AI describes systems where autonomous software “agents” each pursue a defined sub-goal and coordinate, rather than a single end-to-end model. Straight-through processing (STP) means an application is decided automatically with no human touch. Human-in-the-loop (HITL) means a person reviews or approves AI recommendations before they become binding decisions. Deterministic rule engine refers to logic that produces the same output for the same input every time — essential where a regulator needs a traceable, reproducible reason for a decision.

The MENA twist is what much general coverage ignores. An underwriting bot trained on English forms tends to collapse when handed an Egyptian-Arabic medical certificate or a Gulf-dialect broker email. Practical regional automation requires Arabic NLP, bilingual document parsing, and Takaful-specific rule engines. For a broader look at how custom agents handle regulated workflows, see our breakdown of custom AI agent architecture for regulated industries.

How Does AI Automation for Insurance Underwriting Workflow MENA Actually Work?

AI automation for insurance underwriting workflow MENA works by chaining specialized agents that each own one stage of risk assessment, passing structured data forward while flagging edge cases for human review. The system aims to mimic underwriter logic but execute it in seconds rather than days.

Here’s the mechanism in a typical implementation. A broker submits a commercial property application as a 14-page PDF in mixed Arabic and English. An intake agent extracts each field — sums insured, location, construction type, prior claims — using OCR plus large language model parsing. A validation agent cross-checks the address against flood and fire-risk databases and flags inconsistencies. A pricing agent applies the insurer’s rate tables and risk appetite. A compliance agent confirms the structure meets Takaful requirements where applicable. Finally, a decision agent either binds, declines, or escalates to a human underwriter.

A worked example of the trade-offs: suppose the intake agent extracts a “year built” of 1119 from a poorly scanned Arabic document (a common OCR error where an Arabic-Indic numeral is misread). A naive pipeline prices the risk against a nonexistent building age. A well-designed validation agent catches the implausible value, refuses to pass it forward, and routes the case to a human — exactly the kind of guardrail that distinguishes a production system from a demo. Practitioners generally find that most of the engineering effort goes into these validation and exception paths, not the happy path.

“AI and generative AI enable automation and task augmentation that help underwriters handle more tasks, work more efficiently,” according to Accenture’s insurance underwriting analysis. That augmentation framing is the honest one — these systems are positioned to remove the grunt work surrounding the judgment call, not to replace the judgment itself.

eData, positioning itself as a MENA leader, markets “AI agents that mimic underwriter logic while reducing error margins by up to 90%” (eData Management Middle East, LinkedIn, October 2025). It’s worth being precise: this 90% figure is a vendor’s published claim, not an independently audited measurement, and eData does not publish the baseline methodology behind it. The mechanism it points to — eliminating manual transcription and rule-application mistakes — is plausible, but the magnitude will vary widely by data quality and process maturity.

The deterministic layer is what separates robust systems from “AI sycophancy.” A probabilistic model that simply agrees with whatever the broker submitted is dangerous in an underwriting context. Sound underwriting automation uses deterministic rule engines for the compliance-critical steps and reserves the LLM for unstructured extraction. We cover this distinction in our guide to deterministic AI vs. probabilistic yes-machines.

Why Is AI Automation for Insurance Underwriting Workflow MENA Different From Other Regions?

AI automation for insurance underwriting workflow in MENA differs from other regions because of three distinct realities: dual-regulator compliance, Sharia-compliant Takaful logic, and Arabic-language document processing across multiple dialects. Ignore any one of these and the system risks failing an audit or alienating a customer.

Regulatory compliance. Saudi Arabia’s insurance sector is supervised by the Saudi Central Bank, whose framework for insurance governance and risk management is publicly documented. (Readers should consult SAMA’s official insurance supervision publications and the UAE Central Bank’s insurance rulebook directly for the current, binding text, as these instruments are periodically revised.) Both regimes broadly require explainable decisions and audit trails. An autonomous AI that approves a policy without a traceable reason chain is a regulatory liability. That’s why human-in-the-loop architecture isn’t optional in MENA — it’s structural. Where this article references regulatory expectations, treat them as a starting point for your own legal review, not as legal advice.

Takaful insurance. Takaful is a Sharia-compliant cooperative insurance model where participants contribute to a shared pool rather than transferring risk to a profit-seeking insurer. Underwriting rules differ: no interest-based (riba) calculations, no investment in prohibited (haram) sectors, and surplus-distribution logic that returns part of any pool surplus to participants. A generic pricing agent built for conventional insurance can produce non-compliant outputs. The rule engine has to encode Takaful constraints natively, and ideally the logic should be reviewable by a Sharia supervisory board within your organization.

Arabic document processing. MENA underwriting documents arrive in Modern Standard Arabic, Gulf dialect, Egyptian dialect, Levantine and Maghrebi variants, and code-switched Arabic-English. OCR and NLP pipelines trained primarily on English tend to degrade on Arabic script, right-to-left layouts, ligatures, and dialectal variation. Practitioners generally find that document-extraction accuracy — not model reasoning — is the single biggest determinant of a project’s success in the region.

On market context: the MENA insurance market continues to grow, with Gulf states pursuing digitization mandates under Saudi Vision 2030 and the UAE’s digital economy strategy. We deliberately avoid citing a precise market-size figure here because we could not verify one against a primary source; readers wanting hard numbers should consult published regulator and industry-body reports directly. For the broader augmentation case, the Accenture insurance underwriting research lays it out clearly.

What Are the Measurable Benefits of AI Underwriting Automation?

AI underwriting automation is associated with benefits in three core areas: error reduction, capacity gains, and faster turnaround. Below, each claim is anchored to a cited source and clearly labelled as either a vendor claim or a logical consequence of the workflow design — not presented as an established fact.

- Error reduction (vendor claim — up to 90%): eData markets AI agents that reduce error margins by up to 90% by removing manual transcription and rule-application mistakes (eData, October 2025). Independent verification is not available; treat as a marketing figure.

- More in-appetite business (vendor claim — 40%+): mea Platform’s Intelligent Underwriting products are marketed as helping underwriters “write over 40 percent more in-appetite business with no extra effort” (mea Platform / Financial IT).

- Faster turnaround (mechanistic): When straight-through processing applies and only edge cases escalate, applications that took 3–5 days for manual review can resolve in minutes. This follows directly from parallelizing intake and validation; the exact saving depends on your STP eligibility rate.

- Lower loss ratios (mechanistic): Consistent rule application reduces mispriced policies, tightening the gap between expected and actual claims — though this benefit only appears if your rules were correct to begin with.

- Underwriter retention (qualitative): Removing repetitive data entry lets skilled underwriters focus on complex risks. This is a frequently reported soft benefit, but we are aware of no published, region-specific quantification of it.

The honest trade-off: these benefits only materialize with clean data pipelines and proper validation. Garbage in still produces garbage out — faster. A team that skips the validation agent to save time can end up auto-binding bad risks at scale, a far costlier mistake than slow manual review. This is why the vendor headline numbers above should be read as best-case marketing, not guarantees.

How to verify benefits for yourself: the only credible figure is the one you measure against your own baseline. Before automating, sample a few hundred recent manual decisions, calculate your actual error and rework rate, and record your average cycle time. After deployment, re-measure the same cohort. That before/after comparison — not a vendor slide — is what you can defend to your board and your regulator. To model the financial return, our AI ROI calculator frames error-cost savings and capacity gains for brokers and insurers.

Should You Build Custom AI Underwriting Agents or Buy an Off-the-Shelf Platform?

The build-vs-buy decision in MENA underwriting is genuinely close, and anyone who tells you one option always wins is selling something. Custom AI underwriting agents tend to make sense when off-the-shelf platforms can’t meet your requirements — deep ERP integration with legacy core systems, Takaful-specific rule logic, or Arabic dialect handling across Gulf, Levantine, and Maghrebi variants. Buying a platform like mea or eData tends to win when speed-to-deploy matters more than customization and your workflows are standard.

Here’s an honest comparison. The figures below are illustrative ranges drawn from how such projects generally scope out; your actual numbers will depend on integration complexity and document volume, so validate them with vendor quotes and internal estimates rather than treating them as fixed.

| Factor | Custom AI Agents | Off-the-Shelf Platform (mea, eData) |

|---|---|---|

| Time to deploy (typical) | Longer — months, not weeks | Shorter — weeks for standard lines |

| Takaful rule logic | Fully customizable, native | Depends on vendor; often retrofitted |

| Arabic dialect handling | Tuned to your document mix | Generic Arabic support |

| ERP / core system integration | Deep, bidirectional | API-limited, sometimes constrained |

| Upfront cost | Higher one-time build | Lower start, recurring SaaS fees |

| Long-term cost | You own it — no per-seat fee | Scales with users/policies |

| Auditability for SAMA / UAE regulator | Designed for your regulator | Vendor-controlled logic |

mea Platform markets “pre-built agentic AI that automates submission, clearance, and policy workflows to cut costs and speed bind” (mea Platform). For a mid-sized broker with standard motor and property lines, that pre-built speed is genuinely attractive — there’s little sense in rebuilding what already works.

The counter-consideration is recurring cost and control. Off-the-shelf platforms typically charge per seat or per policy, and those fees compound as you grow. A custom agent — built once, owned, and integrated directly into your existing ERP — removes the recurring fee but carries higher upfront cost and maintenance responsibility. For Takaful operators and insurers with non-standard products, the custom path also avoids forcing a unique workflow into someone else’s template. Neither path is universally correct.

A practical starting point: map your actual workflow first. If roughly 80% of it is standard, a hybrid approach often wins — buy the commodity intake layer, build the compliance and pricing agents that encode your competitive edge. Validate that split with a small pilot before committing capital either way.

How Do You Implement AI Underwriting Automation in 90 Days?

A realistic AI underwriting automation rollout can fit a three-phase, roughly 90-day structure for a contained scope: weeks 1–4 for data and workflow mapping, weeks 5–8 for agent development and testing, and weeks 9–12 for human-in-the-loop deployment and tuning. Larger, multi-line or multi-jurisdiction programmes typically run longer. Rushing the data phase is the most common failure mode practitioners report.

Follow this practical sequence:

- Weeks 1–4 — Map and clean. Document your current four-stage workflow. Identify which application types are high-volume and standard (good automation candidates) versus complex and judgment-heavy (keep human-led). Audit your document sources, including Arabic dialect distribution, and — critically — measure your existing manual error and cycle-time baseline so you have a defensible “before.”

- Weeks 5–8 — Build the agents. Develop the intake, validation, pricing, and compliance agents. Encode your regulator’s audit requirements and Takaful constraints into the deterministic rule engine. Test against historical applications where the correct outcome is already known, and have a Sharia supervisory reviewer sign off on Takaful logic.

- Weeks 9–12 — Deploy with humans in the loop. Start in shadow mode: the AI recommends, the human decides. Measure agreement rates. Once the system matches underwriter decisions on a high proportion of standard cases, enable straight-through processing for low-risk auto-approvals while routing edge cases to humans.

The human-in-the-loop design is the heart of compliant MENA automation. As a rule, never let the AI auto-decline a customer without a human checkpoint — regulators and reputations both suffer when an opaque model rejects someone wrongly. The right balance auto-approves the obvious yes-cases, auto-flags the obvious fraud, and escalates everything ambiguous.

One actionable warning that recurs across implementations: measure your baseline error rate before you automate. If you can’t show the manual process had, say, a 6% error rate, you cannot credibly claim the AI dropped it to 0.6%. Document the before so you can defend the after — this is also how you sanity-check vendor claims like the 90% figure against your own reality.

Key Takeaways

- AI automation for insurance underwriting workflow MENA follows a four-stage model: ingest, validate, apply rules, trigger actions.

- Agentic AI — multiple specialized agents — is the dominant emerging architecture, prized for auditability.

- Headline gains (up to 90% error reduction from eData; 40%+ more in-appetite business from mea Platform) are vendor marketing claims, not independently audited results — verify against your own baseline.

- MENA-specific requirements — SAMA/UAE regulator compliance, Takaful logic, Arabic dialect processing — make generic platforms risky.

- Human-in-the-loop architecture is structural, not optional, for regulatory compliance.

- Build custom for ERP depth and Takaful logic; buy off-the-shelf for speed on standard lines; consider a hybrid.

Frequently Asked Questions

What is the four-stage automated underwriting workflow?

The four-stage automated underwriting workflow consists of ingesting application data, validating it for accuracy and fraud, applying business and compliance rules, and triggering downstream actions like approval or escalation. This structure is a widely cited industry standard for AI underwriting automation and provides clear handoff points for human oversight.

Can AI underwriting automation handle Sharia-compliant Takaful insurance?

Yes, but only when the rule engine natively encodes Takaful constraints — no interest-based calculations, no prohibited-sector exposure, and proper surplus-distribution logic, ideally reviewed by a Sharia supervisory board. Generic platforms built for conventional insurance often produce non-compliant outputs, which is why custom-built agents are frequently preferred for Takaful operators in MENA markets.

Does AI replace insurance underwriters in MENA?

No. AI automation augments underwriters rather than replacing them, handling repetitive data entry, validation, and standard rule application while human underwriters focus on complex risks and final decisions. Accenture notes that AI “help[s] underwriters handle more tasks, work more efficiently” — augmentation, not replacement, is the prevailing model.

How much error reduction can AI underwriting automation deliver?

MENA-focused provider eData markets up to a 90% reduction in error margins by deploying AI agents that mimic underwriter logic (October 2025). This is a vendor claim rather than an independently audited benchmark; actual results depend heavily on data quality, baseline error rates, and validation-agent design. Measure your own before/after to know what you’ll get.

What regulators govern AI underwriting in Saudi Arabia and the UAE?

Saudi Arabia’s insurance underwriting is supervised by the Saudi Central Bank (SAMA), while the UAE’s insurance sector falls under the Central Bank of the UAE’s framework. Both broadly require explainable decisions and complete audit trails, making human-in-the-loop architecture and deterministic rule engines essential. Consult the regulators’ official, current publications directly, as these rules are periodically updated.

The Bottom Line

The MENA insurers likely to lead over the next five years aren’t the ones with the flashiest AI demos — they’re the ones who quietly rebuild their underwriting workflow around agents that respect SAMA and the UAE regulator, process Arabic accurately, and encode Takaful logic correctly. The technology is maturing fast. But the often-quoted 90% error reduction and 40% capacity gains are vendor marketing figures, not laws of nature — they materialize only with clean data, deterministic rules where compliance demands it, and a human in the loop where judgment matters. Build it with that discipline, measure against an honest baseline, and underwriting can shift from bottleneck to advantage.

Sources & References

- eData Management Middle East — MENA insurance automation announcement (LinkedIn, 19 October 2025) — source of the “up to 90% error reduction” vendor claim.

- mea Platform — Agentic AI for (Re)Insurance Operations — pre-built agentic AI for submission, clearance, and policy workflows.

- mea Platform / Financial IT — new AI products for core insurance workflows — source of the “40%+ more in-appetite business” vendor claim.

- Accenture — AI is the transformative technology for underwriting — the augmentation (vs. replacement) framing.

- InsurTech Gulf — Agentic AI in underwriting: multi-agent systems — the multi-agent lifecycle model.

- OpenAI — Research & Deployment — general background on the large language models underpinning intake/extraction agents.

Note: This article is for general informational purposes; verify specifics against your own context.